You can track the Twin Cities housing market data here. You can track mortgage rates here. You can track homebuilder confidence here. You can track showing activity here. You can track lumber prices here.

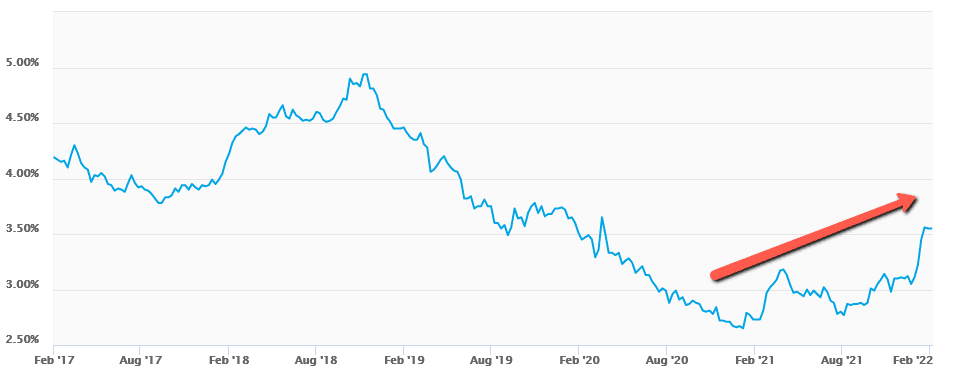

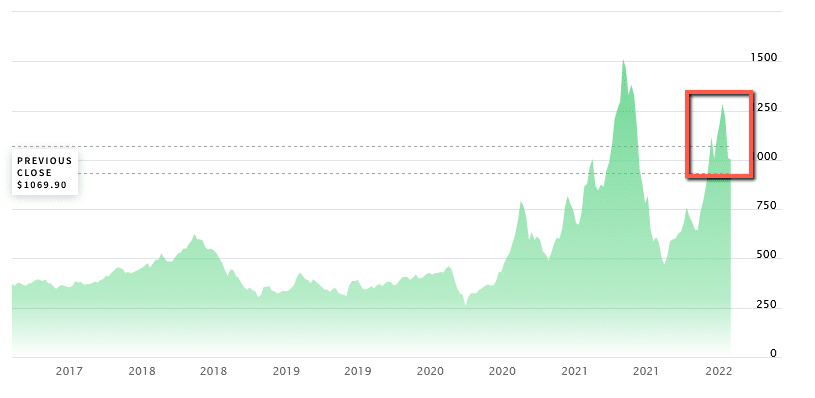

Mortgage rates moved up 15% in January to near a 2-year high, as the bond market priced in an anticipated 5 Fed rate hikes in 2022.

Hiking interest rates into a slowing economy has historically been very bad for the U.S. stock market. In recent history (the dotcom bust of the early 2000s, the 2008 financial crisis, the 2018 stock market crash and the 2020 stock market crash), crashing stock prices have been very dovish for monetary policy as the Federal Reserve has consistently used monetary intervention (QE & artificially low rates) to support "the economy" or better put, to support asset prices. With evidence of an economic slow down in 2022 starting to emerge, one could speculate that the tightening the Fed is about to embark on is likely to cause or contribute to a crash (as defined by a fall of 20% or greater from a stock's peak) in U.S. equities, the pricing in of which appears to have already begun. As of Monday, the S&P 500 is down 5.82% from its January peak, the Nasdaq is down 12% from its November peak, the Russell 2000 is down 17% from its November peak and Bitcoin is down 36% from its November peak. Some of the higher risk, more speculative tech stocks which have benefited greatly from the 0% interest rate environment, have been flash crashing with facebook (the largest collapse in valuation of a U.S. company in history) and Snap, Inc. both falling 26% in a single day.

If the Fed moves forward with their rate hike plans and if economic data in 2022 starts coming in unfavorable, as it looks like it may, U.S. equity prices are likely to enter "crash" territory which would put the Fed in a very difficult position in having to choose between fighting inflation by tightening monetary policy or fighting recession (A.K.A. supporting asset prices) by keeping 0% interest rates and QE in place. Getting rising inflation under control in a central bank managed economy has historically required a long and painful process of bringing interest rates well above the rate of inflation for a sustained period of time. With debt levels (government, consumer, business, mortgage and student) all at record highs, I believe there is currently more political pressure to keep the easy money flowing than there is political pressure to get inflation under control, so my speculation, at least for 2022, is that the Fed will eventually be forced by the market to abandon the inflation fight and return to the dovish policies that got us here, not necessarily because it’s the right thing to do, but because the process of getting Americans psychologically and financially prepared for the pain that must actually be endured to get inflation under control, is politically nonviable.

There is no question that a significant and sustained increase in mortgage rates would have a downward impact on housing affordability and therefore a downward impact on housing demand. According to research from Hedgeye Risk Management, mortgage rates need to rise 75 basis points (or ¾ of a percentage point) before they begin to impact affordability in a meaningful enough way to affect housing prices. With that said, that conclusion was derived from studying more balanced markets in terms of supply and demand fundamentals.

Since August of 2021, the 30-year mortgage rate has risen 85 basis points (from 2.65% to 3.5%) so it has certainly risen enough to have an impact, however, while mortgage rates were rising in January, home inventory in the Twin Cities continued to fall, down another 6% MOM to a new record low. The housing market is currently so significantly under-supplied ahead of the peak season (for a majority of market segments) that I believe home prices in the Twin Cities will continue to rise during the first half of 2022, regardless of a rising interest rate headwind, just maybe not as much as they would have otherwise risen had mortgage rates remained under 2.75% or under 3%.

Conclusion: I believe the Fed is likely to abandon their rate hike plans in the face of falling stock prices which would likely result in mortgage rates coming back down at some point this year. However, even if the Fed doesn't back off, while rising mortgage rates will undoubtedly impact housing affordability and therefore demand, because the supply and demand fundamentals are so heavily distorted towards sellers to start this year's market cycle, rising mortgage rates will likely only dampen the rate of increase but will not be able to prevent home prices from rising during the first half of 2022.

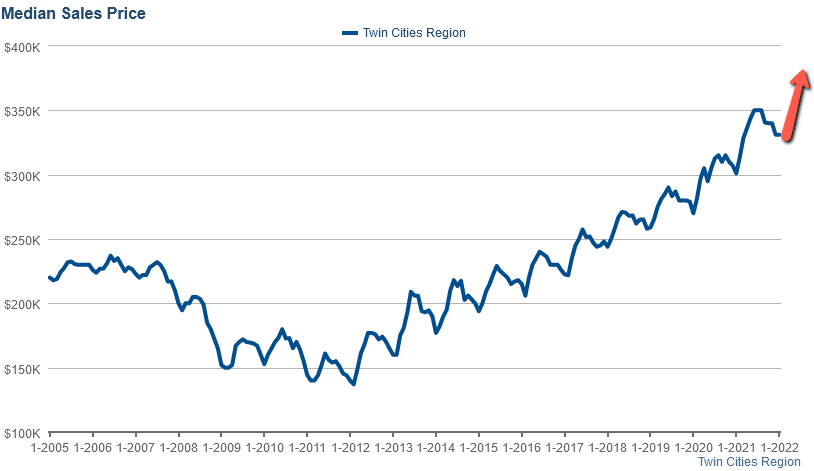

The Median Home Price: The median home price in the Twin Cities stayed flat at $331,000 in January which is likely the bottom of this winter correction cycle. With inventory sitting at a record low 4,000 units in the Twin Cities, the stage is set for another inflationary spring for home prices, despite rising interest rates.

Hiking interest rates into a slowing economy has historically been very bad for the U.S. stock market. In recent history (the dotcom bust of the early 2000s, the 2008 financial crisis, the 2018 stock market crash and the 2020 stock market crash), crashing stock prices have been very dovish for monetary policy as the Federal Reserve has consistently used monetary intervention (QE & artificially low rates) to support "the economy" or better put, to support asset prices. With evidence of an economic slow down in 2022 starting to emerge, one could speculate that the tightening the Fed is about to embark on is likely to cause or contribute to a crash (as defined by a fall of 20% or greater from a stock's peak) in U.S. equities, the pricing in of which appears to have already begun. As of Monday, the S&P 500 is down 5.82% from its January peak, the Nasdaq is down 12% from its November peak, the Russell 2000 is down 17% from its November peak and Bitcoin is down 36% from its November peak. Some of the higher risk, more speculative tech stocks which have benefited greatly from the 0% interest rate environment, have been flash crashing with facebook (the largest collapse in valuation of a U.S. company in history) and Snap, Inc. both falling 26% in a single day.

If the Fed moves forward with their rate hike plans and if economic data in 2022 starts coming in unfavorable, as it looks like it may, U.S. equity prices are likely to enter "crash" territory which would put the Fed in a very difficult position in having to choose between fighting inflation by tightening monetary policy or fighting recession (A.K.A. supporting asset prices) by keeping 0% interest rates and QE in place. Getting rising inflation under control in a central bank managed economy has historically required a long and painful process of bringing interest rates well above the rate of inflation for a sustained period of time. With debt levels (government, consumer, business, mortgage and student) all at record highs, I believe there is currently more political pressure to keep the easy money flowing than there is political pressure to get inflation under control, so my speculation, at least for 2022, is that the Fed will eventually be forced by the market to abandon the inflation fight and return to the dovish policies that got us here, not necessarily because it’s the right thing to do, but because the process of getting Americans psychologically and financially prepared for the pain that must actually be endured to get inflation under control, is politically nonviable.

There is no question that a significant and sustained increase in mortgage rates would have a downward impact on housing affordability and therefore a downward impact on housing demand. According to research from Hedgeye Risk Management, mortgage rates need to rise 75 basis points (or ¾ of a percentage point) before they begin to impact affordability in a meaningful enough way to affect housing prices. With that said, that conclusion was derived from studying more balanced markets in terms of supply and demand fundamentals.

Since August of 2021, the 30-year mortgage rate has risen 85 basis points (from 2.65% to 3.5%) so it has certainly risen enough to have an impact, however, while mortgage rates were rising in January, home inventory in the Twin Cities continued to fall, down another 6% MOM to a new record low. The housing market is currently so significantly under-supplied ahead of the peak season (for a majority of market segments) that I believe home prices in the Twin Cities will continue to rise during the first half of 2022, regardless of a rising interest rate headwind, just maybe not as much as they would have otherwise risen had mortgage rates remained under 2.75% or under 3%.

Conclusion: I believe the Fed is likely to abandon their rate hike plans in the face of falling stock prices which would likely result in mortgage rates coming back down at some point this year. However, even if the Fed doesn't back off, while rising mortgage rates will undoubtedly impact housing affordability and therefore demand, because the supply and demand fundamentals are so heavily distorted towards sellers to start this year's market cycle, rising mortgage rates will likely only dampen the rate of increase but will not be able to prevent home prices from rising during the first half of 2022.

The Median Home Price: The median home price in the Twin Cities stayed flat at $331,000 in January which is likely the bottom of this winter correction cycle. With inventory sitting at a record low 4,000 units in the Twin Cities, the stage is set for another inflationary spring for home prices, despite rising interest rates.

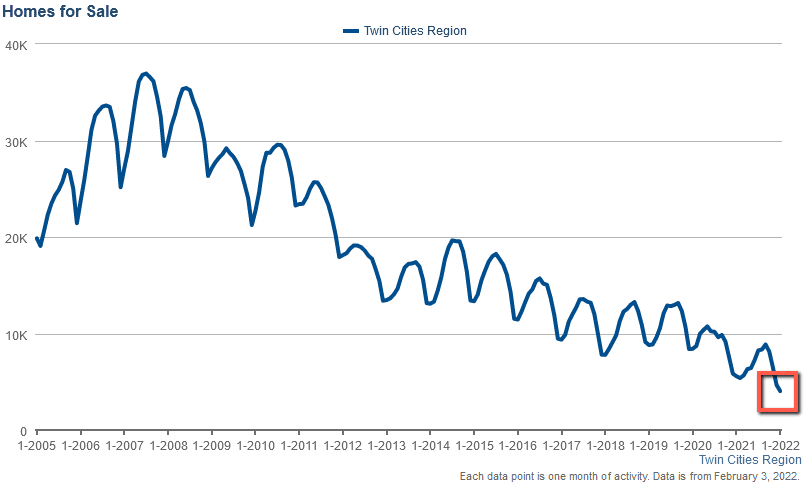

Home Inventory: Home inventory fell 6% in January and down 20% YOY to yet another record low of 4,033 units. That record is likely stand for some time because January inventory is typically the cycle bottom. The overall inventory is set to rise as both buy and sell activity increases until the next seasonal peak in late summer/early fall.

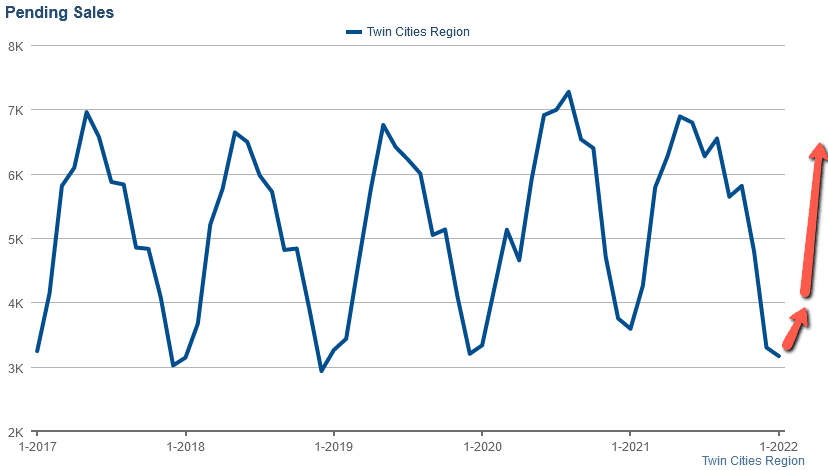

Pending Home Sales: Pending sales fell 3% in January to 3,164 units which is also likely a cycle bottom. We expect demand to move up significantly in February as the spring market of 2022 kicks into gear.

Mortgage Rates: Mortgage rates moved up 15% in January to 3.55% for the average 30-year-fixed conventional mortgage in the U.S. That rate represents almost a 2 year high and is up 85 basis points YoY from when a 30-year-fixed mortgage was locking in at 2.65%.

Lumber Prices: Lumber prices were very volatile in January. They moved up another 15% and then fell 30% to end the month down 15% MOM. That is still a 180% increase from pre-pandemic prices.

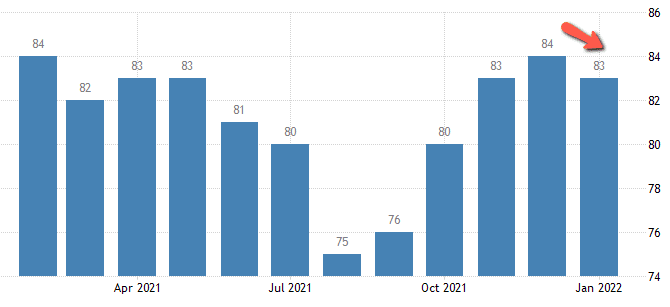

Home Builder Confidence: The NAHB housing market index in the US fell by 1 point to 83 in January of 2022 from a 10-month high of 84 in December which was slightly below market forecasts of 84.

This concludes my Twin Cities housing market insight for February of 2022. Please don't hesitate to call us at (952) 222-7653 if you would like to go more in depth on a particular market segment or dive into the current fair market value of a property that you currently own or manage.

Sources: NorthstarMLS, Hedgeeye Risk Management, FreddieMac.com, Nasdaq.com, TradingEconomics.com